Is It Possible to Have Positive Cash Flow and Negative Net Income?

Companies with a high or uptrending operating cash flow are generally considered to be in good financial health. Many line items in the cash flow statement do not belong in the operating activities section. Cash flow from operating activities is an important benchmark to determine the financial https://careers.whittard.co.uk/2020/03/24/the-abcs-of-zero-coupon-bonds/ success of a company’s core business activities. Cash flow from operating activities does not include long-term capital expenditures or investment revenue and expense. CFO focuses only on the core business, and is also known as operating cash flow (OCF) or net cash from operating activities.

Operating Cash Flow

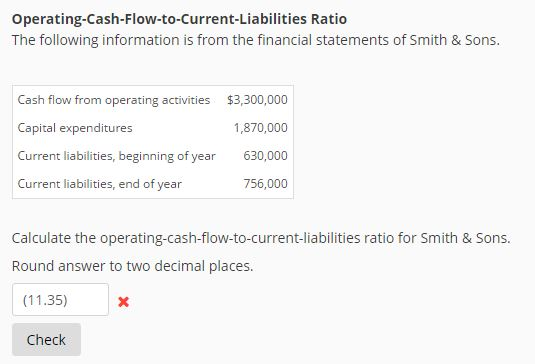

If the ratio is less than 1, the company generated less cash from operations than is needed to pay off its short-term liabilities. A higher ratio – greater than 1.0 – is preferred by investors, creditors, and analysts, as it means a company can cover its current short-term liabilities and still have earnings left over.

But if you continue to earn a strong operating profit, it’s most likely a matter of time before you can turn around your cash flow and bring your balance sheet back into positive territory. The first item on the https://en.wikipedia.org/wiki/Retained_earnings income statement is revenue, or cash from sales, and subtracted from that are the expenses and depreciation. Then you have to calculate the tax paid, which you do by multiplying the business’s tax rate by EBIT.

Cash flow definition

What is a good return on equity?

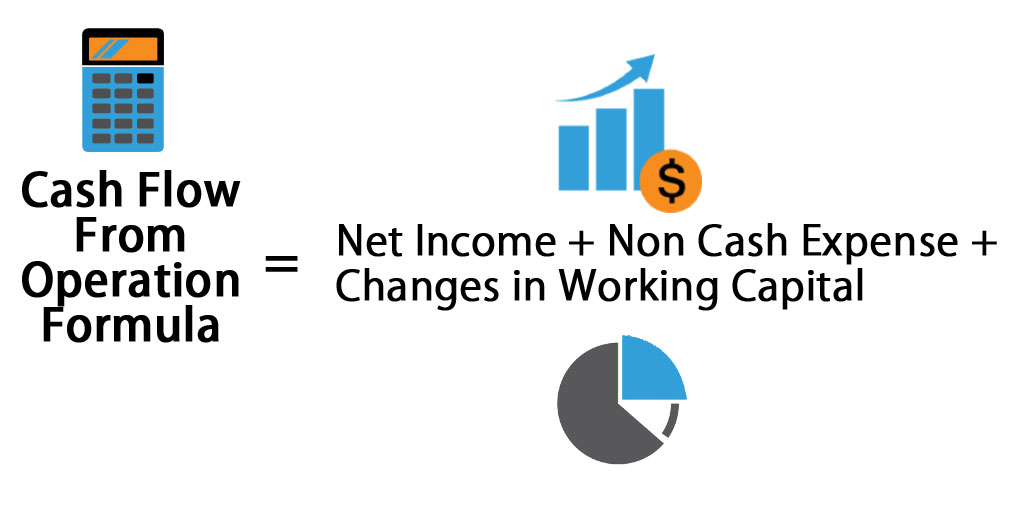

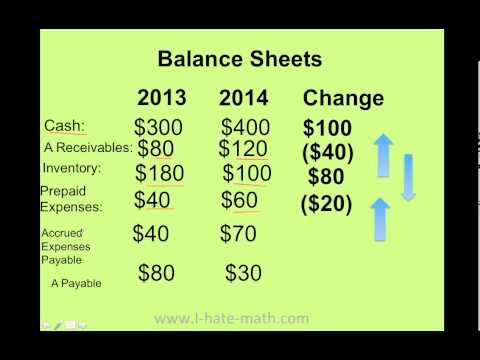

If balance of an asset increases, cash flow from operations will decrease. If balance of an asset decreases, cash flow from operations will increase. If balance of a liability increases, cash flow from operations will increase. If balance of a liability decreases, cash flow from operations will decrease.

The cash flow statement uses cash basis accounting instead of accrual basis accounting which is used for the balance sheet and income statement by most companies. This is important because a company may accrue accounting revenues but may not actually receive the cash. This could produce profits and taxes payable but not provide the resources to stay solvent. cash equivalents Because the cash flow statement only counts liquid assets in the form of cash and cash equivalents, it makes adjustments to operating income in order to arrive at the net change in cash. Depreciation and amortization expense appear on the income statement in order to give a realistic picture of the decreasing value of assets over their useful life.

Negative Cash Flow Statements

- Therefore, while net income could be negative, the cash flow would show a gain.

- The CFS can help determine whether a company has enough liquidity or cash to pay its expenses.

- In other words, if you send an invoice in June that isn’t paid in September, you’ll mark that as “collections onaccounts receivable” in September.

Operating cash flows, however, only consider transactions that impact cash, so these adjustments are reversed. Financing and investment activities https://yandex.ru/search/?text=??????%20????????&lr=213 are excluded because the purpose of the operating cash flow is to segregate and evaluate the health of the normal operations or core business.

This enables it to settle debts, reinvest in its business, return money to shareholders, pay expenses, and provide a buffer against future financial challenges. What may not be apparent from a review of these documents is how they relate to each other.

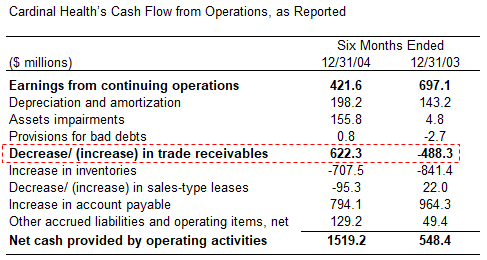

The depreciation accounting entries are to debit depreciation expense and credit accumulated depreciation, which reduces the book value of fixed assets on the balance sheet. For example, if a small business has a $5,000 computer on its books, the annual depreciation expense over https://en.forexpamm.info/ its estimated five-year useful life is $5,000 divided by 5, or $1,000. This expense will reduce net income, but it will be added back to operating cash flow because it is a non-cash expense. Therefore, while net income could be negative, the cash flow would show a gain.

Operating Cash Flow (OCF)

The tax paid is then subtracted from the EBIT, and then the depreciation is added back in. Companies with strong financial flexibility can take advantage of profitable investments. They also fare https://www.google.ru/search?newwindow=1&biw=1434&bih=742&ei=E-cMXsGkApHrrgTap6WQCQ&q=metatrader+4&oq=metatrader+4&gs_l=psy-ab.3..0i71l8.212362.212362..212464…0.2..0.0.0…….0….2j1..gws-wiz.l_s7_N0_0bk&ved=0ahUKEwiB-qiHhuPmAhWRtYsKHdpTCZIQ4dUDCAo&uact=5 better in downturns, by avoiding the costs of financial distress. Assessing the amounts, timing, and uncertainty of cash flows is one of the most basic objectives of financial reporting.

For instance, the interest expense reported on your company’s income statement reduces the amount of cash recorded on the related cash flow statement. Your operating profit margin gives a quick glance at the overall financial health of your company’s operations. It plays a part in your overall financial status but it does not tell the whole story. If you lost money or made major equipment purchases in a previous year, you may be struggling to pay back these sums, even if your operating profit is solid.

Understanding the cash flow statement – which reports operating cash flow, investing cash flow, and financing cash flow — is essential for assessing a company’s liquidity, flexibility, and overall financial performance. The three categories of cash flows are operating activities, investing activities, and financing activities.

How do you get cash flow?

ROE is especially used for comparing the performance of companies in the same industry. As with return on capital, a ROE is a measure of management’s ability to generate income from the equity available to it. ROEs of 15-20% are generally considered good.